-

Without increased support to develop renewable energy in Southeast Asia, the affordability of electricity and renewable hydrogen will be at risk.

Given the early stage of renewable energy deployment in the region, countries should prioritise renewable energy and supporting infrastructure such as grids and system flexibility. Cross-sectoral policy frameworks for renewables and hydrogen that include robust environmental and social standards can attract potential investors and create new jobs.

-

Southeast Asian countries should avoid overestimating their role as renewable hydrogen exporters in the dynamic global Power-to-X (PtX) market.

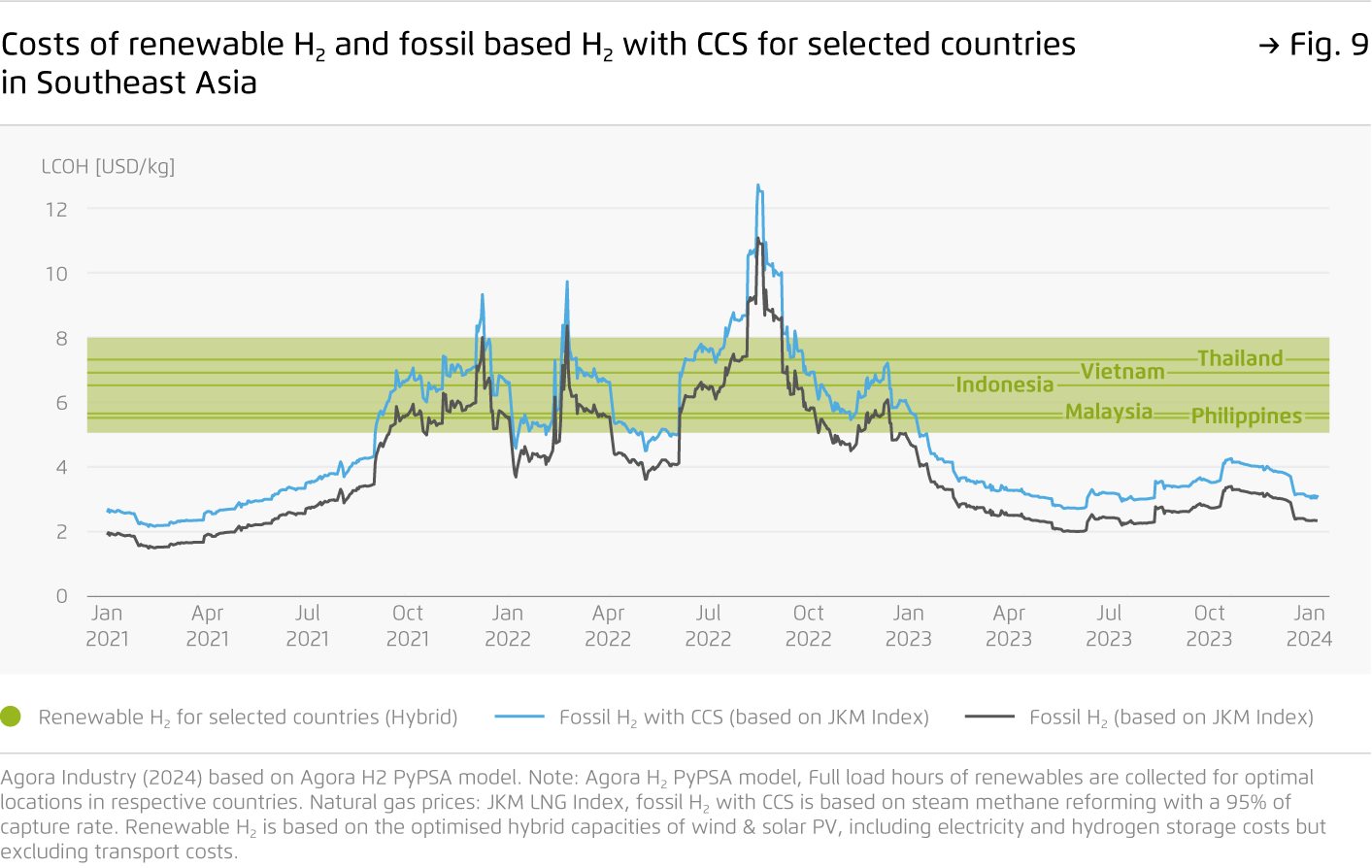

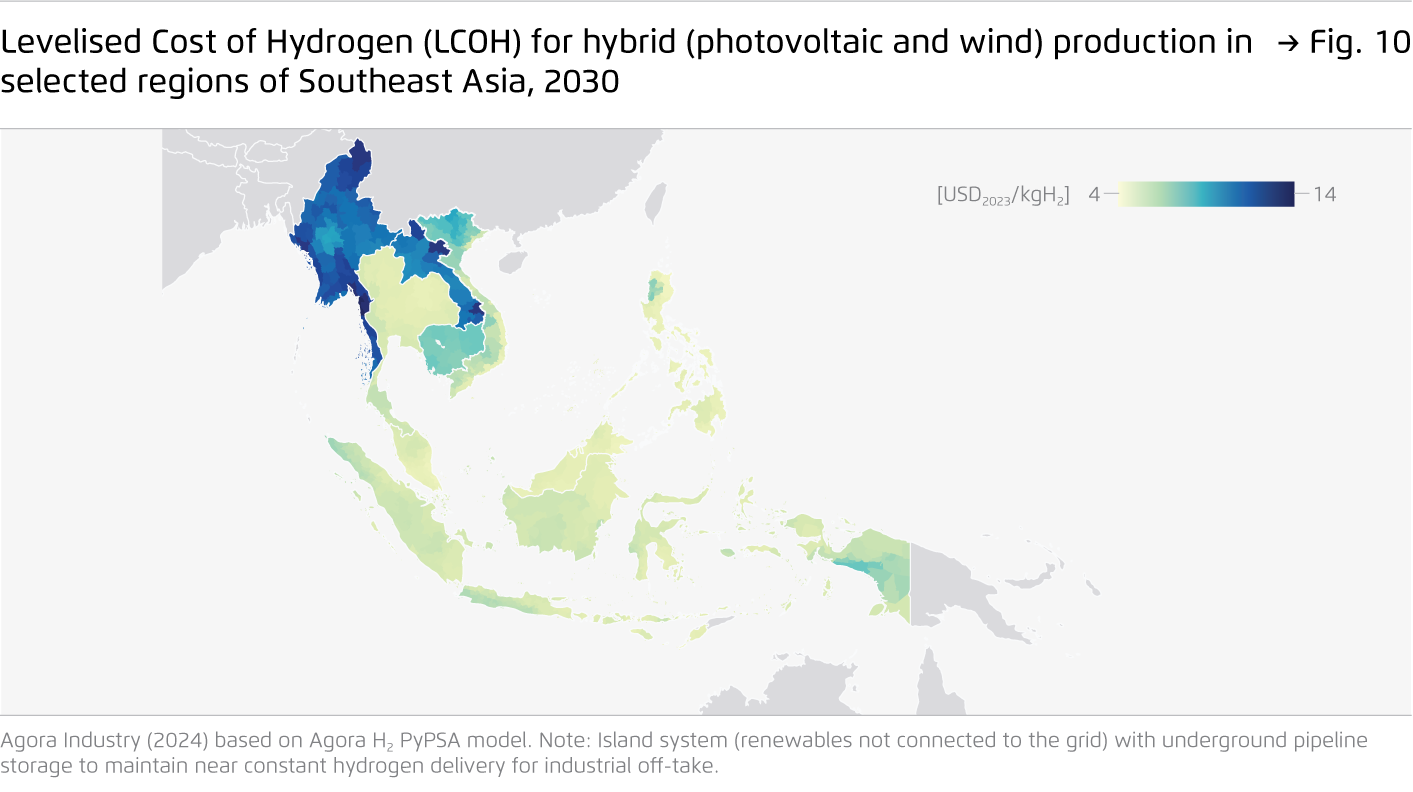

Despite having ample renewable resources to meet domestic energy needs, hydrogen costs are not as competitive compared to other potential exporting regions. Embracing a “global gas hub” strategy, as advocated by some Southeast Asian countries, could risk stranding infrastructures. Nevertheless, proximity to East Asian markets could increase Southeast Asia’s potential for PtX trade through strategic partnerships.

-

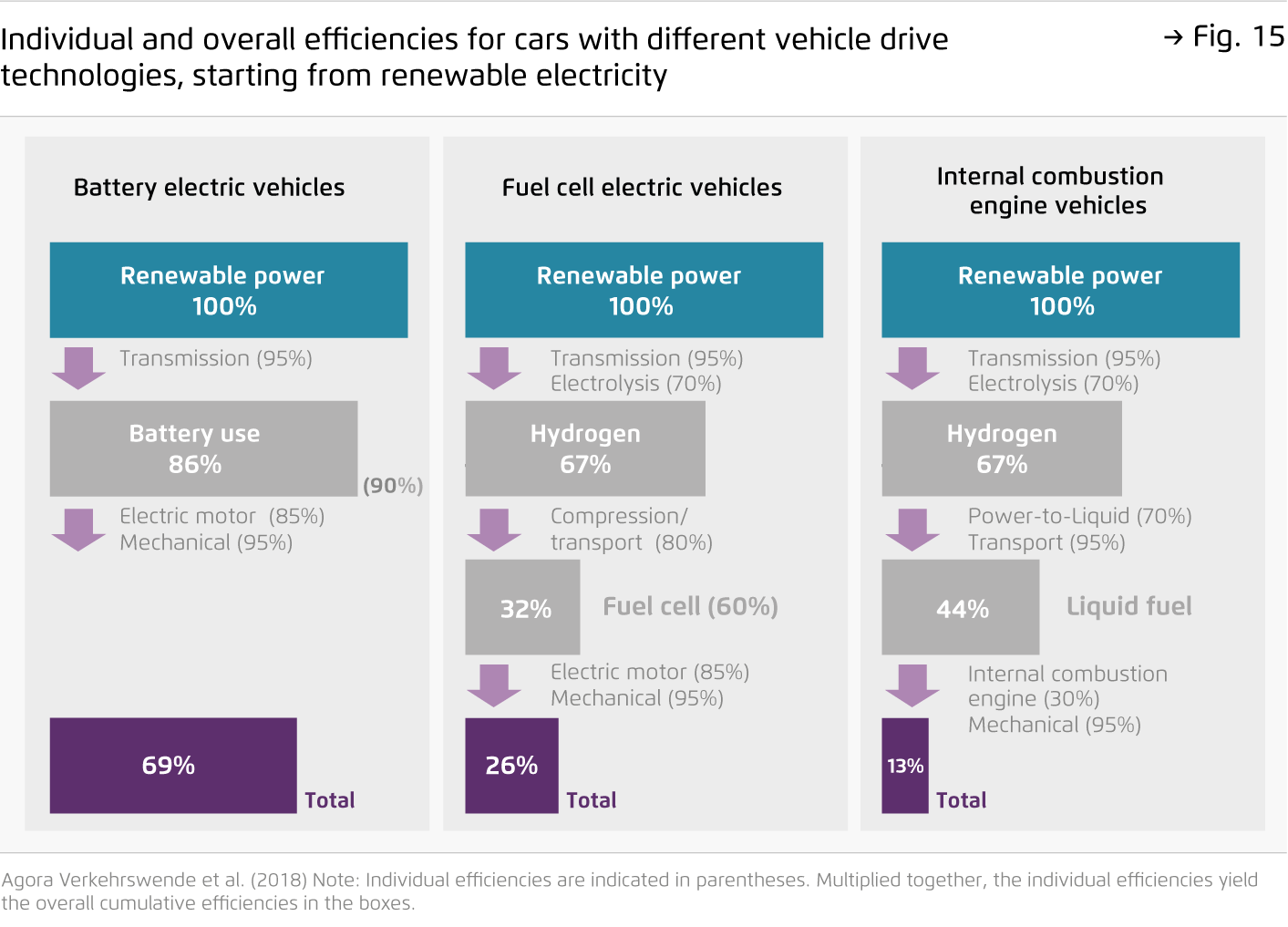

Low-carbon hydrogen should be reserved for ‘no regret’ applications where no electrification alternatives exist.

Southeast Asian countries should focus on decarbonising demand by switching from fossil fuels to electricity wherever possible. Hydrogen is better suited to decarbonise heavy industries such as steel, while proposed applications such as ammonia coal co-firing are cost inefficient and ineffective in reducing emissions.

-

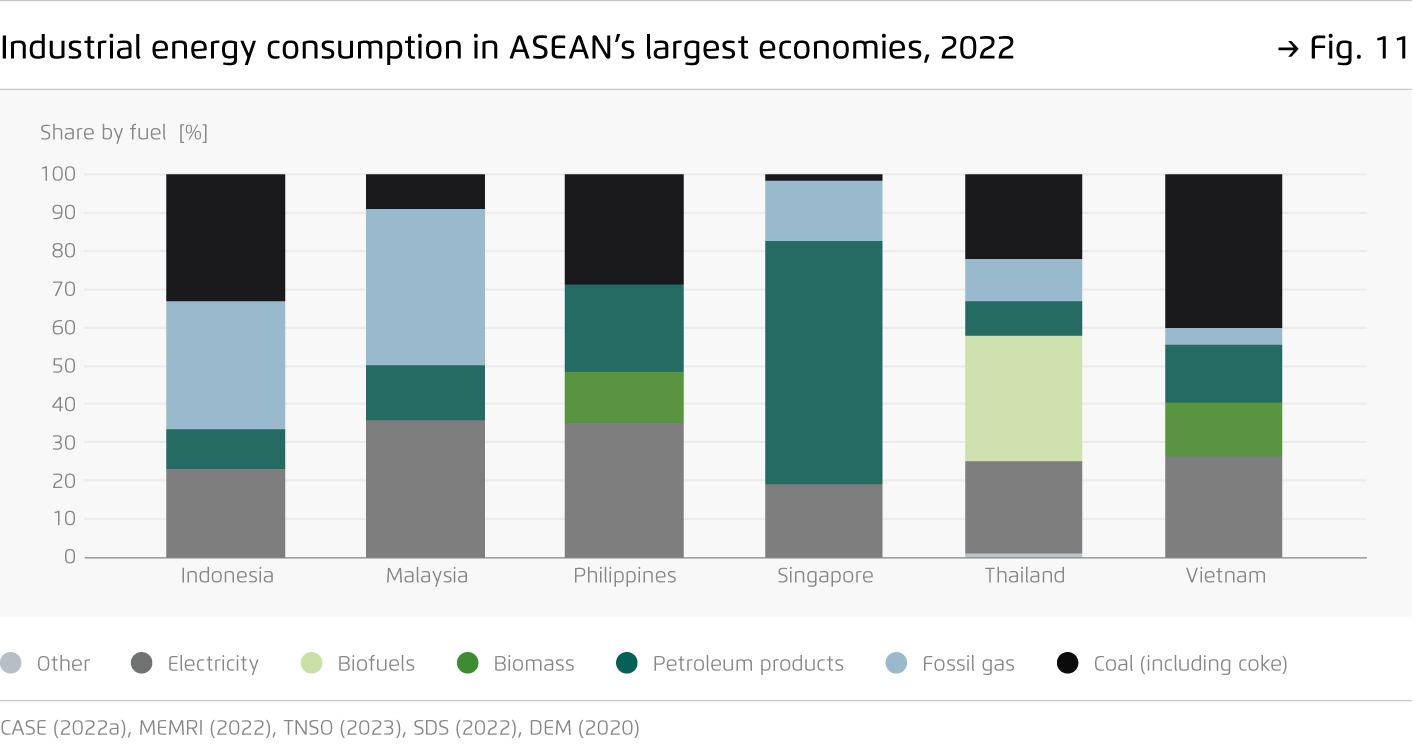

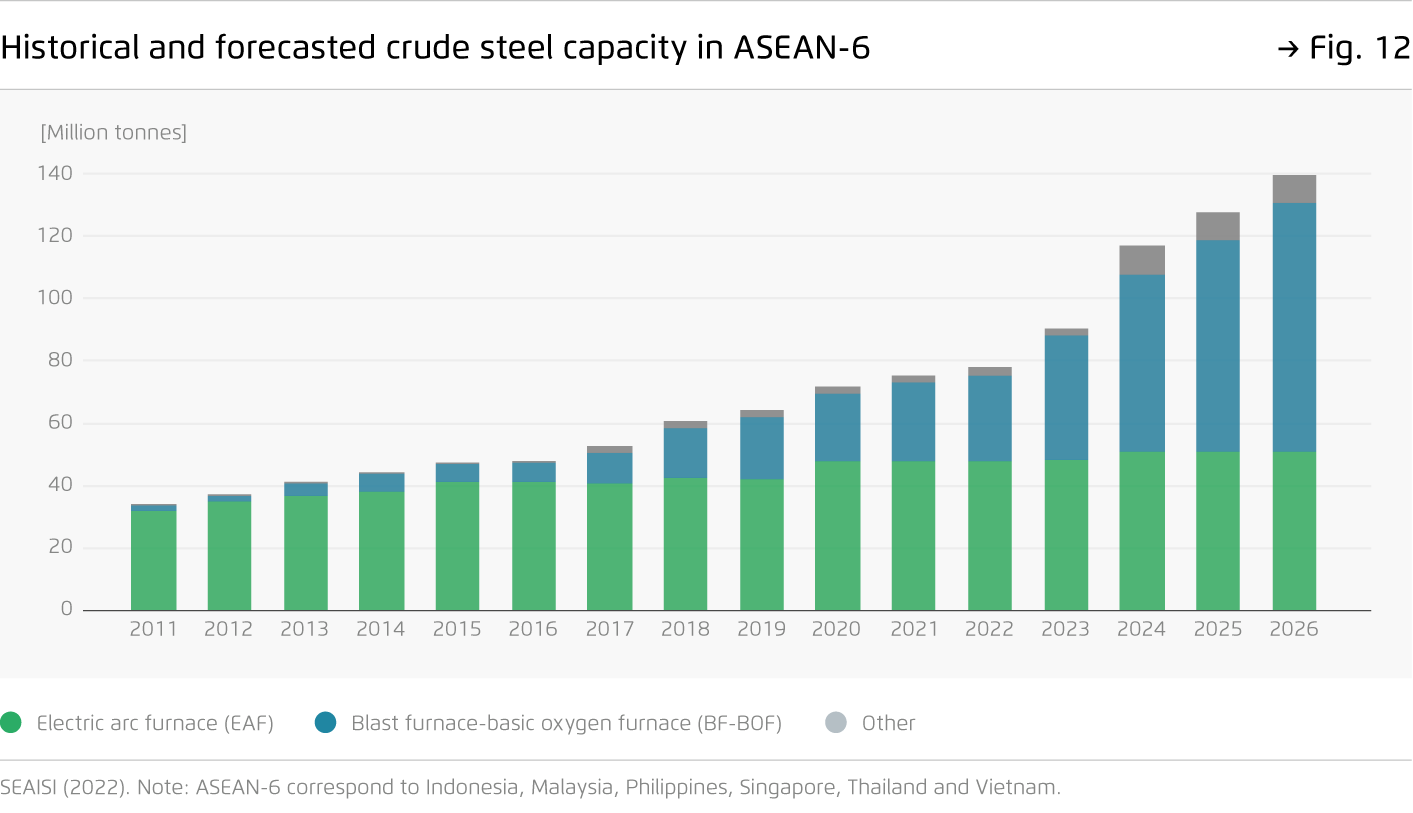

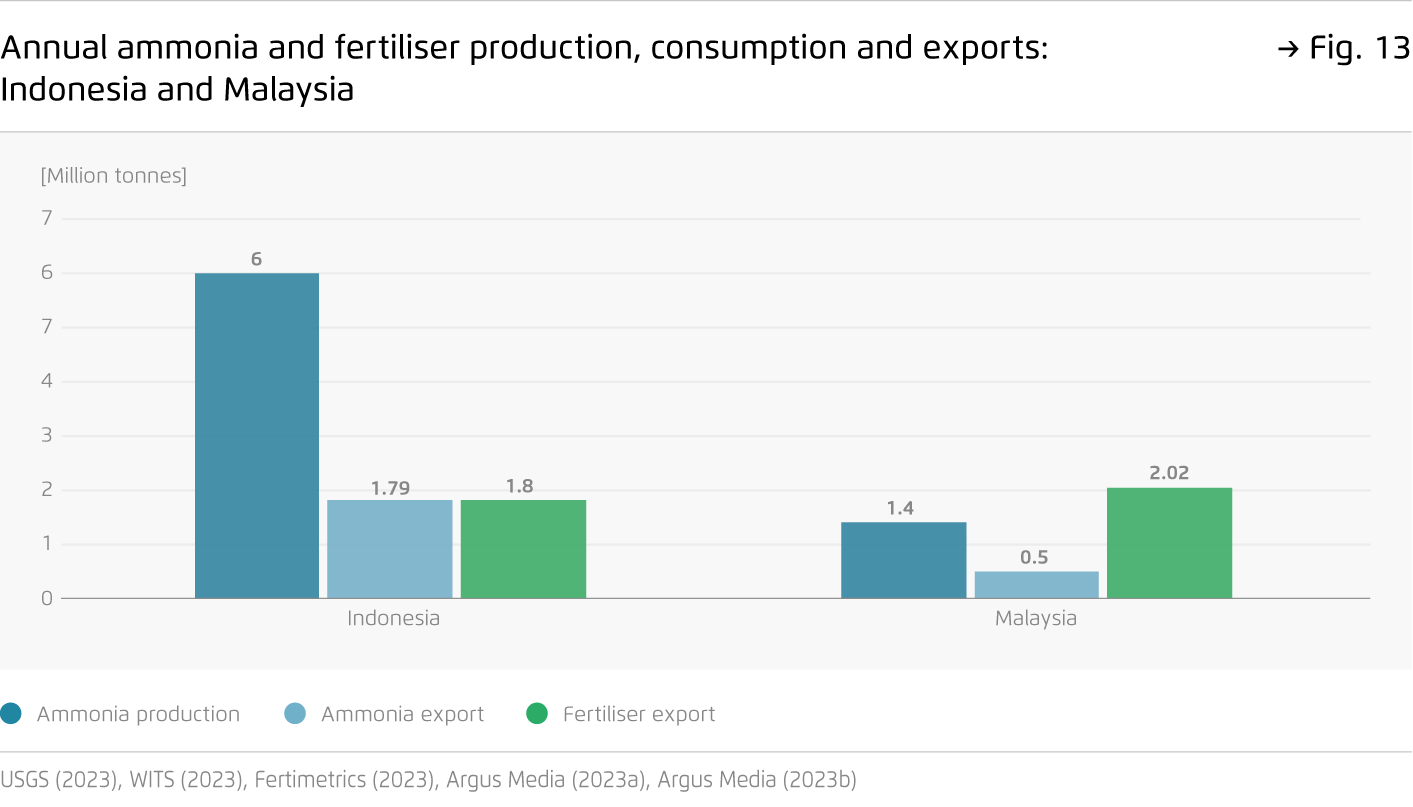

Southeast Asia’s rapidly growing heavy industries offer a timely opportunity to establish a low-carbon industrial sector.

Using renewable hydrogen for non-energy use in industrial processes such as steel, ammonia and fertiliser production can open the region to global low-carbon markets and avoid significant emissions. Future prospects for direct electrification may offer more efficient solutions than hydrogen, even for high-temperature heat in industry or heavy-duty vehicles.

9 insights on hydrogen – Southeast Asia edition

A contribution to the debate over hydrogen in Southeast Asia as the region seeks to align its rapid economic development with ambitious climate targets.

Preface

With most countries in Southeast Asia having adopted net-zero emissions targets, domestic and regional policy discussions have started to explore pathways that can realise these commitments. Hydrogen has generated an enormous amount of attention over the past few years: over 50 countries have published hydrogen strategies and many others, including those in Southeast Asia, intend to do so soon.

However, how hydrogen fits into national decarbonisation strategies remains uncertain. In the power sector, the use of ammonia coal co-firing to reduce emissions is being discussed. In the industrial sector, a wave of new investments in steel production could trigger additional dynamic demand for hydrogen.

On the supply side, the region is expected to soon become a net importer of fossil gas. At the same time, the development of renewable energy is still at an early stage and needs to be accelerated.

This report aims to inform discussions on priorities and ‘no regret’ uses of hydrogen specific to the Southeast Asian context. In addition to exploring different pathways of hydrogen demand and supply, it also examines the opportunities and challenges for energy infrastructure and Southeast Asia’s position in the global hydrogen trade. We hope this will help to provide evidence to galvanise discussions around hydrogen throughout the region.

Key findings

Bibliographical data

All figures in this publication

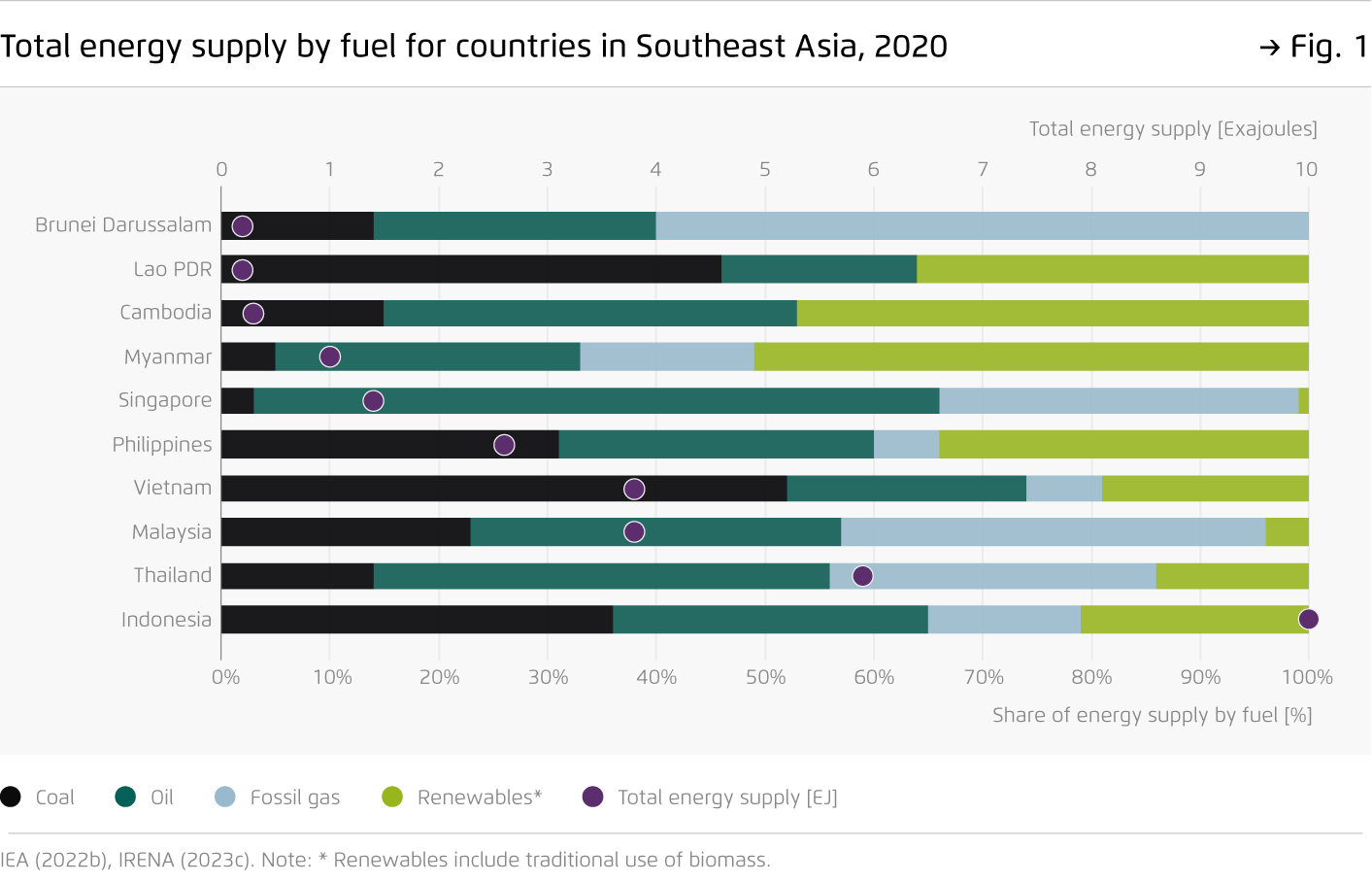

Total energy supply by fuel for countries in Southeast Asia, 2020

Figure 1 from 9 insights on hydrogen – Southeast Asia edition on page 5

Estimates of global hydrogen demand in 2050: selected scenarios

Figure 2 from 9 insights on hydrogen – Southeast Asia edition on page 7

![[Translate to English:] How Argentina can become a renewable hydrogen hub and boost global decarbonisation](/fileadmin/_processed_/8/c/csm_news_4d473bf99c.jpg)